This is a joint diary by Bonddad and New Deal democrat.

In December 2008, with the economy and employment in freefall, NDD asked Is there Hope for an Obama Economic Recovery in 2009? After noting that " This is an economy in free-fall" and that "a Deflationary Bust -- the first since 1938 -- is in full force, " I wrote that

Left to its own devices, I suspect the economy would succumb to a deflationary spiral. But Ben Bernanke and the Federal Reserve know this as well: Bernanke is a scholar of Federal Reserve mistakes during the 1929-32 Great Depression. He is resolved not to make the same mistakes that were made then.

....

There is at least some hope [that] ....a new Administration in Washington populated by Economic Adults may unfreeze the logjam of money supply sitting in banks and not being lent out. Certainly there is a pressing need for massive infrastructure investments that can lead to renewed bank lending and economic expansion on Main Street.

Yes there is Hope for an Obama Economic Recovery in 2009.

Yesterday the non-partisan NBER confirmed that is exactly what happened.

Yesterday the NBER, the official arbiter of economic cycles in the US, declared that the bottom of the "Great Recession" occurred in June 2009 and a recovery from that bottom began the next month. Coming less than 45 days from the midterm elections, it could hardly have been better timing for democrats, who can now contrast their policies which helped this country rebound from the depths of its worst economic downturn since the Great Depression, against the teatard madness of the GOP.

I. What we said

The NBER declaration is also a vindication of the economic analysis that used to be regularly available on this blog from myself and from New Deal democrat.

On November 30, 2007, as it turns out the day before the official start of the "Great Recession", NDD wrote that The Panic of 2008? predicting:

This is NOT the Great Depression II. Nor is this the stagflationary 1970s. It is going to unfold as some other Beast. Only the broad outlines of this Beast appear discernable now: it will likely feature (1) increasing import prices; (2) wage stagnation (that does not keep up with price inflation; (3) real asset deflation; and (4) possibly a Japan-style "liquidity trap."

That turned out to be almost a perfect description of exactly what did subsequently happen.

Thereafter, because the 2007-2009 economic downturn had much in common with the Great Depression, and because very few statistical series cover that period of time, in<span style="font-weight:bold;"> in January 2009 </span>in a series of 5 posts, NDD examined "Economic Indicators during the Roaring Twenties and Great Depression" in detail. Noting that the Great Depression as well as the 1938 recession, and other recessions during the 1920s had bottomed when the rate of YoY change in prices bottomed, NDD concluded:

the indicators we have studied from the earlier Deflationary period suggest that the recession might bottom out in about Q3

By April, it was reasonably clear that a wage deflationary spiral was not going to happen, and that gave confidence enough to write:

For purposes of this discussion, I am going to assume that the optimistic scenario turns out to be the correct one: viz., that the YoY inflation rate will bottom in about July 2009 and that will mark the end of the recession and the beginning point of any recovery.

By early May 2009 we had had both a bottom in retail sales, stabilization in the housing market, and the signs of significant decline in both initial jobless claims and monthly payroll losses. On May 07, NDD wrote:

This week's decline increases the likelihood that the recession is very close to bottoming to more than 50%.

[This]is not the only indication that the recession may be close to bottoming out.... Last Friday the ISM Manufacturing Index for April was released. It was all but ignored in the economic blogosphere.... In summary, the NAPM Manufacturing index's reading for April is consistent with the recession bottoming out, and a recovery beginning almost immediately.....

.... the NBER may ultimately date the end of this recession from June or July of this year.

Four days later, referring primarily to the Leading Economic Indicators, which were almost all showing signs of turning upward, we jointly wrote

there are plenty of reasons, those listed above not being in any way exhaustive, that people like us are saying that the economic situation looks like it is getting ready to improve.

For my part, throughout the summer, I continued to note the improvement in the numbers. On June 29th I wrote, The Recovery is On the Horizon where he noted,

Doom sells. When someone says "the sky is falling" it's easy to say "yes it is -- and we're all just plain going to hell." However, the data points of the last 3-4 months indicate the economy is bottoming. In addition, the leading economic indicators tell us the possibility of recovery is very high. Let's look at what the data says.

On July 8, 2009 I wrote, The Economic Freefall is Over where he noted,

Gloom and doom is the way of blogs lately. Nothing is good; everything is bad. Unfortunately, lost in this translation is a set of monthly trends that shows the worse is over. Now -- this does not mean everything is roses. Far from it. As I have mentioned in the past the recovery will be weak with slow growth and high (7%-8% minimum) unemployment for the better part of a year. But the data indicates the worst is behind us.

Finally, on July 18 I wrote:

The economic news this week added further evidence to the story that the economy is bottoming. While we are not out of the woods yet (by a long shot) the worst is behind us.

By the end of August we were both confident, and correct, enough to write bluntly that This Recession is Over.<div>

II. The NBER's reasoning

In declaring that the recession bottomed in mid 2009, the NBER said:

In determining that a trough occurred in June 2009, the committee did not conclude that economic conditions since that month have been favorable or that the economy has returned to operating at normal capacity. Rather, the committee determined only that the recession ended and a recovery began in that month. A recession is a period of falling economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales. The trough marks the end of the declining phase and the start of the rising phase of the business cycle. Economic activity is typically below normal in the early stages of an expansion, and it sometimes remains so well into the expansion.

(my emphasis)

Many times there are semantic arguments on this blog about the term "recovery." The NBER has just authoritatively stated what one is: the rising phase off the bottom of a recession, nothing more.

The NBER dating committee identified the data it weighed as follows:

Identifying the date of the trough involved weighing the behavior of various indicators of economic activity.... [T]he committee refers to a variety of monthly indicators to choose the months of peaks and troughs. It places particular emphasis on measures that refer to the total economy rather than to particular sectors. These include a measure of monthly GDP ...and GDI [gross domestic income]..., real personal income excluding transfers, the payroll and household measures of total employment, and aggregate hours of work in the total economy. The committee places less emphasis on monthly data series for industrial production and manufacturing-trade sales, because these refer to particular sectors of the economy. Movements in these series can provide useful additional information when the broader measures are ambiguous about the date of the monthly peak or trough.

Let's look at the indicators the NBER used to declare that the Great Recession bottomed at midyear 2009.

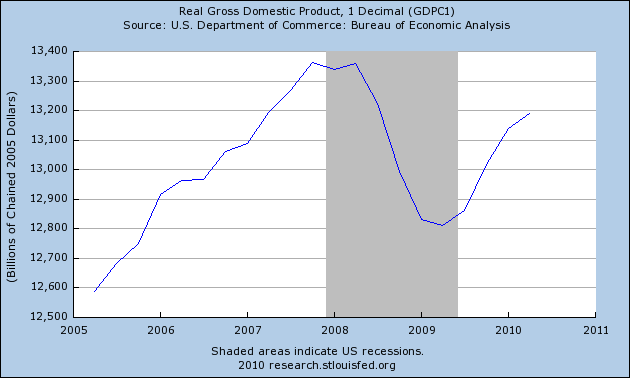

Here's GDP:

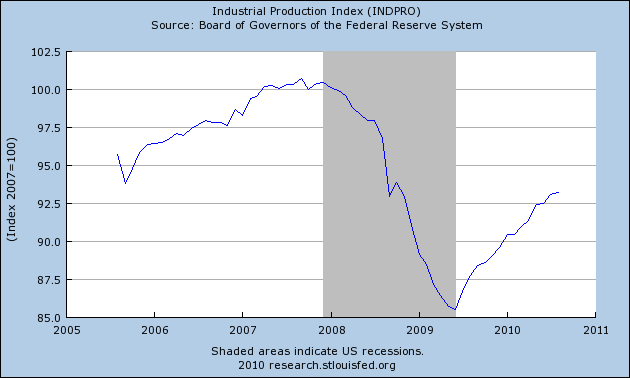

Here is industrial production:

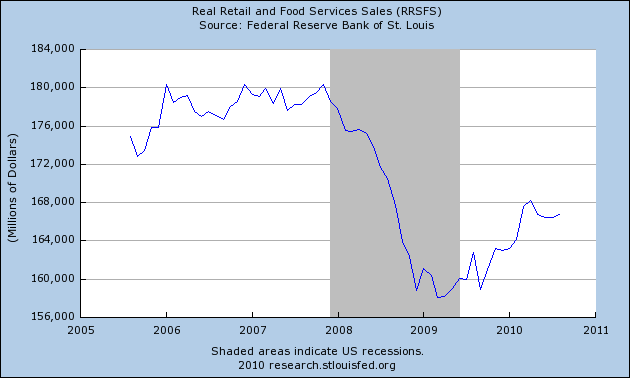

Here are real retail sales:

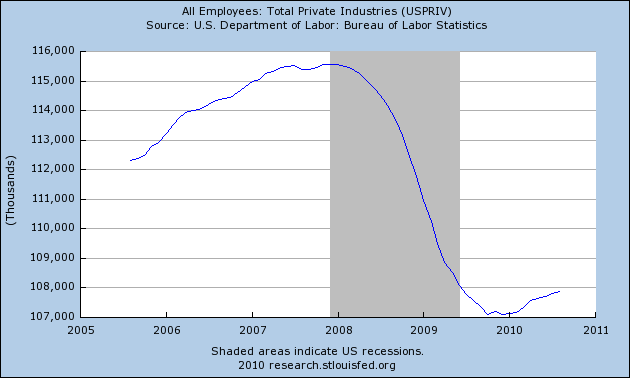

Here are private (non-census) payrolls (these have risen about 600,000 since December 2009:

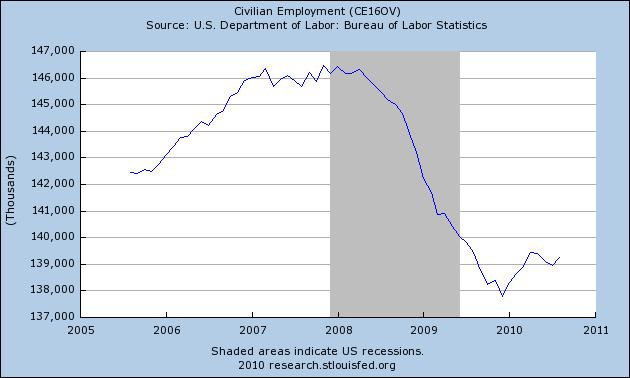

The "establishment survey" in which the BLS calls businesses to survey their hiring and firing isn't the only measure of employment. There is also the "household survey" compiled by surveying households and asking if they have been hired or fired during the last month. It shows about 1.4 million new jobs have been added since December:

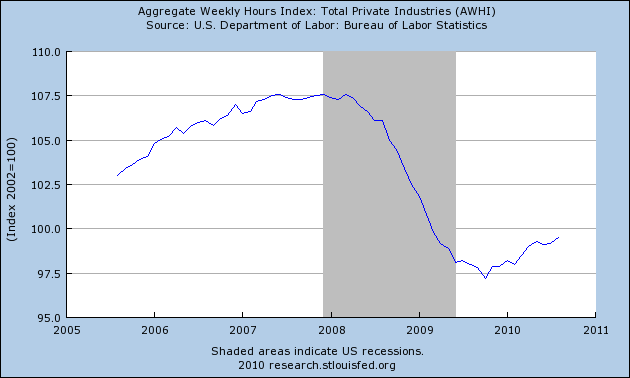

Here are aggregate hours worked in the economy, which measures exactly that. It has risen for a year straight:

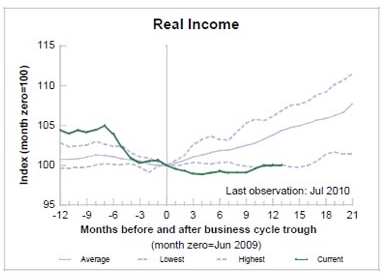

Finally, here is real income, which is the laggard. It has also risen for a year, but pathetically:

In simple terms, what the NBER has declared is that we had a recession until July 2009. We are currently in a recovery because economic activity is expanding. We are not yet in an expansion because that positive economic activity as not yet exceeded its 2007 peak.

III. Econometric data confirms the NBER's call

Prof. James Hamilton of Econbrowser uses a computer-driven algorhythm to generate results, and this morning here is what he had to say:

There are always those who may seize on the political dimension of announcements like this. For example, if you were attempting to assist one party or the other, you might prefer to have the announcement come before or after the election. I maintain that there is value in setting out in advance exactly what one means statistically by the statement "the recession is over", and sticking to that definition.

So what does the statement really tell us? Simply that the economy, as measured by a variety of real economic indicators, has been growing rather than contracting for the last 15 months. Given that historically that condition of economic expansion tends to be highly persistent, in the absence of strong contrary indication, the most likely outcome is that we'll continue to see further economic growth in the months ahead.

There has been some growth in employment, but it has been far too slow to bring the unemployment rate down. And we need stronger GDP growth than I think we are likely to see in the second half of 2010 to make any more progress with the unemployment rate over the rest of this year. I do not think we are currently entering a new recession, though the growth is sufficiently slow, and the lack of more progress on employment sufficiently painful, that it probably still feels very much like a recession to many people.

III. A note about what the Doomers were saying in July 2009:

While we were writing the above, we came under criticism from a DK front pager who claimed that people who held opinioins like ours were "foolish." We were called corporate shills by at least one diarist and it was asserted by another that we were being paid for our work.

At the very time that the NBER has now confirmed that the Recession bottomed, there were Doomers who claimed that it was The End of the End of the Recession touting that

If you're like the rest of us, and you can handle the truth about our economy, here's a quick summary:

....-"...the economy is leaps and bounds away from anything remotely resembling a recovery."

while another in the same month of July derisively claimed that Green Shoots are turning into Brown Weeds:

"Some Green Shoots supporters have declared that the bottom is in. They point towards various short-term trends, and if you don't look too close, it appears to support their cause.... If you look hard enough you can find Green Shoots, but do they actually exist in the real world? Sadly, no..

As late as this July, latching onto a column written by Calculated Risk about the NBER's recession dating (which I also criticized, also correctly as it turned out), one of them claimed:

if another recession starts this year, it will almost certainly be dated as a continuation of the "great recession" that started in 2007....

IMHO, more likely than not, these are the realities of our economy heading into the last four months of the 2010 election cycle.

In short, there can't be a double-dip recession if the Great Recession never ended, in the first place.

Yesterday the NBER settled that debate as well, saying:

The committee decided that any future downturn of the economy would be a new recession and not a continuation of the recession that began in December 2007. The basis for this decision was the length and strength of the recovery to date.

There's a little more revisionist history going on here today, by a diarist who claims to speak for what is helpful to democrats, but nevertheless puts the word "recovery" in scare quotes. So now he spews abuse on the NBER committee. Well, here is the list of the "shills" he now finds it necessary to vilify:

Robert Hall, Stanford University (chair)

Martin Feldstein, Harvard University

Jeffrey Frankel, Harvard University

Robert Gordon, Northwestern University

James Poterba, MIT and NBER President

James Stock, Harvard University

Mark Watson, Princeton University.

Equally shamefully, the diarist quotes GOP economist Arnold Kling approvingly. You may know from that quote just how bad news for the GOP Kling knows the NBER declaration is. It is shameful that his argument should be made on a democratic blog in the middle of an election season where control of both Houses of Congress is in the balance, and shameful that the nonpartisan NBER must be smeared in support of that meme.

V. One debate is over, but the fight to improve average Americans' lives continues

The NBER has now authoritatively settled the acrimonious debate that raged on this blog last year. We were telilng you the truth.

The measures chosen to counter the onset of a "Great Depression 2" are having the desired affect of increasing economic activity, and they have saved - and finally, actually created - jobs in the economy. In other words the downward trend towards the abyss of 2008-early 2009 reversed and became the continually improving upward trend that has continued until now -- niether one of us has said that the absolute level of economic activity, be it of household income, or jobs, or unemployment, or wages, are "good." Thus while in economic terms the "Great Recession" ended last year, "The Hard Times are nowhere near over."

Even though we have come up from the trough, the recovery needs badly to be strengthened, and the safety net for the unemployed vastly improved. As NDD noted in April, the recovery is a gilded one, increasing the maldistribution of wealth between the great mass of Americans, and the corporatocracy of the extremely wealthy. Food stamp usage and extreme poverty are at post world war two highs. A much more populist, Main Street, demand sided economic program remains essential.

And FWIW:

For those of you who are interested in further discussion about the labor market, NDD and I presented two views which you can read here:

http://bonddad.blogspot.com/...

http://bonddad.blogspot.com/...

NDD's rebuttal

http://bonddad.blogspot.com/...

Also note that I called for more infrastructure spending here:

http://bonddad.blogspot.com/...